How will macro and earnings trends influence asset allocation and risk appetite in 2026? This fundamental question will directly determine the opportunity window to increase exposure to risk assets—particularly for equities, credit, and emerging markets.

The Macro Landscape: Steady but Uneven Growth

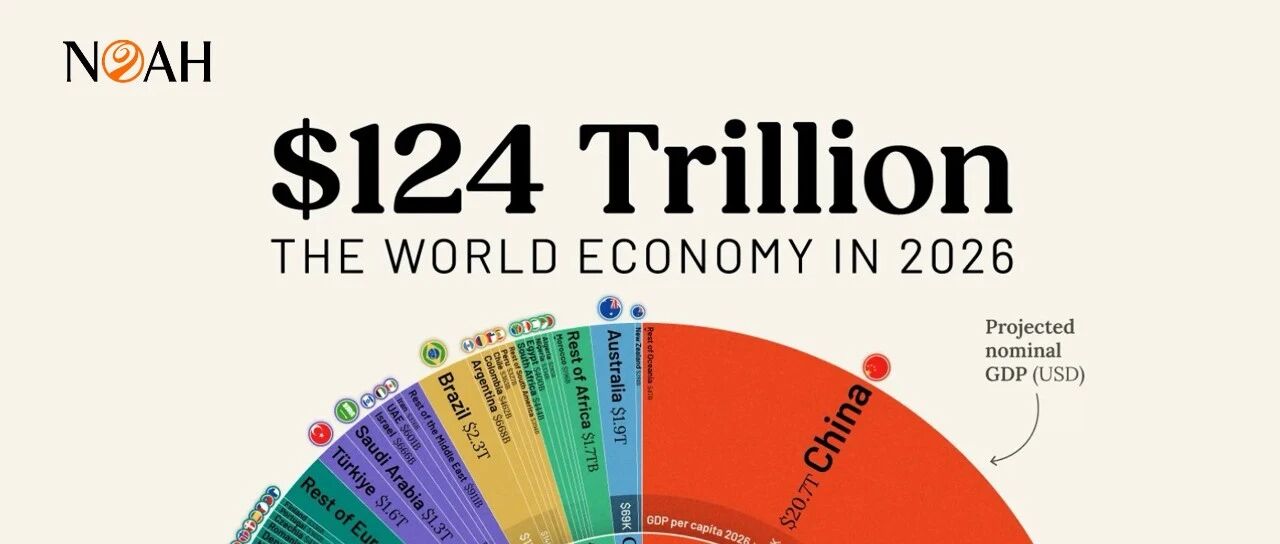

In the latest institutional forecasts, firms such as Goldman Sachs believe the global economy is poised for steady growth of approximately 2.8% in 2026. This projection surpasses market consensus and is expected to be accompanied by a non-recessionary rate-cutting cycle, providing macro support for the continued ascent of risk assets.

However, organizations like the United Nations point out that growth may slow slightly to roughly 2.7%, reflecting how global trade tensions and geopolitical risks continue to suppress potential growth.

Consequently, the Noah CIO Office believes the scenario roadmap can be divided into three paths:

01 Base Scenario

Global GDP ~2.7–2.8% with moderate rate cuts —> Risk appetite improves, while equities and high-grade credit continue to strengthen.

02 Bull Scenario

Faster disinflation and a restart of the European corporate earnings cycle —> Valuation repairs drive regional bull markets, especially in European equities.

03 Bear Scenario

Energy supply shocks or geopolitical risks lead to sticky inflation —> Multiple compression puts risk assets under pressure as macro growth slows alongside policy easing.

Earnings and Valuations: The Core Signal Lights

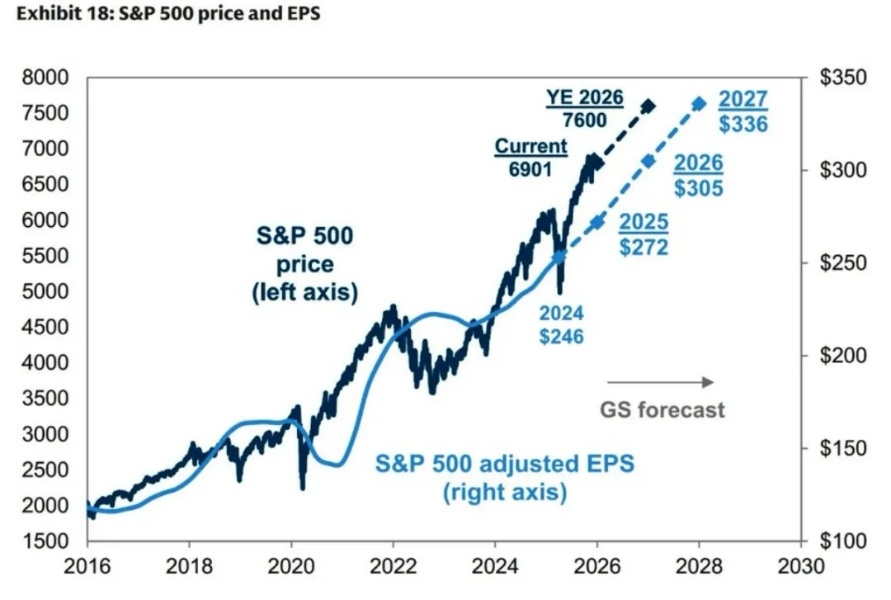

Source: Goldman Sachs Global Investment Research

S&P 500 EPS: Forecasts for 2026 generally hover around US$300.0. This indicates that earnings remain a vital foundation for supporting current valuations.

Growth Potential: While 10.0–15.0% earnings growth is theoretically possible, some strategists warn that growth could "fall below expectations," which would dampen market momentum.

Corporate Earnings Divergence (US vs Europe):

Firms like UBS suggest that after years of stagnation, European corporate earnings growth is expected to recover by approximately 7.0% in 2026, or even higher in 2027. This recovery is a linchpin for the "Bull Scenario."

Strategy Signals and Allocation Variables

Based on these judgments, the Noah CIO Office suggests monitoring three key indicators to guide allocation timing:

01 S&P 500 EPS Trends

If EPS continues to be revised upward —> risk appetite will accelerate, warranting a higher equity ratio.

If EPS is revised downward —> investors should shift toward defensive positions, favoring credit or value/undervalued assets.

02 Central Bank Policy Paths (ECB/BOE/Fed)

A rate-cutting pace faster than expected —> drives valuation expansion, benefiting growth and high-valuation sectors.

Conversely, more cautious policy or a rebound in inflation —> favors yield-generating and defensive assets.

03 Regional Earnings Divergence

Acceleration in European earnings (as predicted by UBS) —> provides a signal to rotate from a "US-centric" focus toward a "US + Europe/EM" strategy.

Asset Allocation for High-Net-Worth and Global Portfolios

Equity vs Credit: If earnings remain stable and the non-recessionary rate-cutting cycle persists, the equity risk premium remains attractive. Otherwise, high-grade credit yields may offer more stability.

US vs EM: S&P 500 earnings support is the key, keeping the US as the core. However, when emerging markets (EM) and European equities show signs of acceleration and greater upside potential, a weighted rotation should be considered.

Infrastructure vs Real Estate: In a scenario of rate cuts combined with earnings improvement, infrastructure—especially energy and AI/digital infrastructure—likely stands to benefit more. Conversely, if inflation remains sticky, the defensive cash flow of real estate will become more prominent.

If these signals light up simultaneously—upward earnings revisions, sustained rate cuts, and robust EPS growth—it represents a clear window to increase exposure to risk assets. Conversely, signs of weakening earnings or tightening policy should trigger a shift toward defense and credit yields.

This streamlined framework is designed to help Noah's high-net-worth clients determine when to adjust positions and how to pivot across regions and asset classes in a dynamic market.